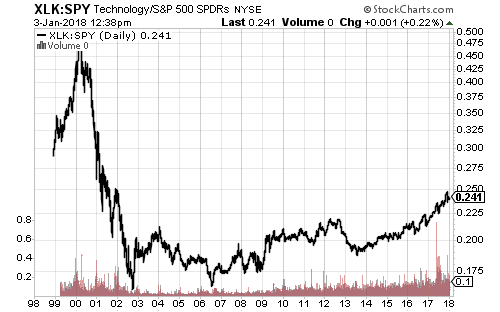

Technology had a great run in 2017, but relative to the broader market, it is currently trading at much lower levels.

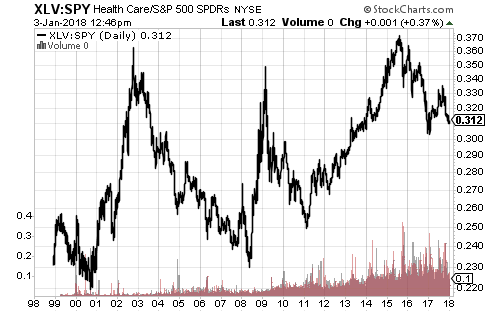

The healthcare sector peaked in 2015 relative to the S&P 500 and has since trailed the market. Pharmaceuticals weighed in 2017, but a reversal could support another era of healthcare outperformance.

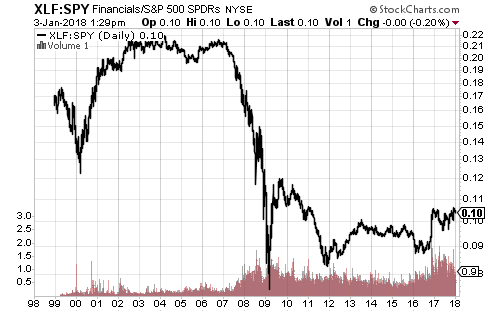

Although the Fed raised rates three times in 2017, financials weakened into June before recovering. Deregulation and/or rising credit growth should lift the sector in 2018. On relative terms, it remains one of the best bargains in the market.

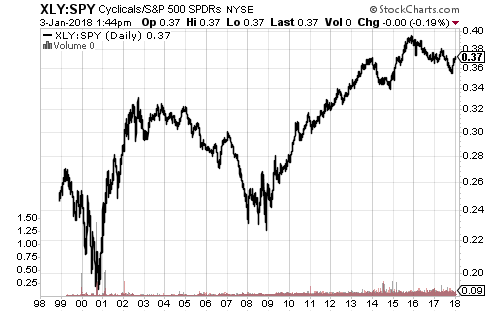

Consumer discretionary outperformed the S&P 500 Index for seven straight years before correcting in 2016 and 2017. Shares of XLY have climbed from a dividend-adjusted $15 in 2009 to a new all-time high of $100 today. Subsectors like physical retail have suffered, but Amazon (AMZN) offset some last year’s weakness. It is now the largest stock at 16.8 percent of assets.

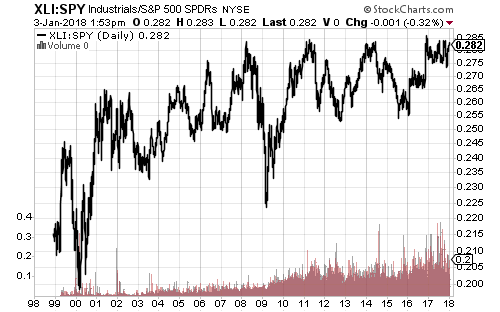

Industrials have been in a long-term uptrend versus the broader market, despite a relative valuation trading range since the start of 2011. A substantial drop in General Electric (GE) last year weighed on the sector. Pro-manufacturing policies from the Trump administration are the biggest potential catalyst for this sector.

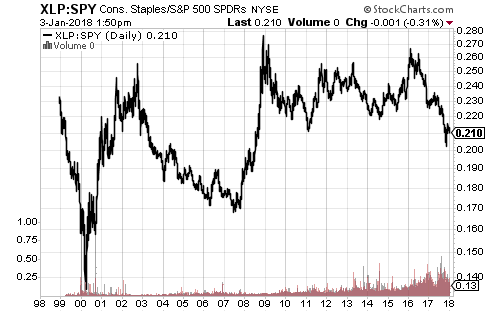

Since the Federal Reserve started raising interest rates at the end of 2015, consumer staples have underperformed the broader market. Investors are hawkish coming into 2018, however.

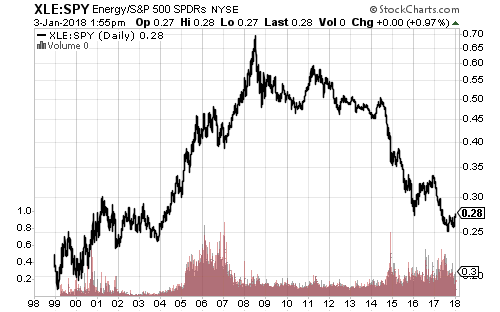

Energy is trading at a steep relative discount to the broader stock market. If oil prices rise in 2017, energy should be among the top performing sectors as valuations catch-up.

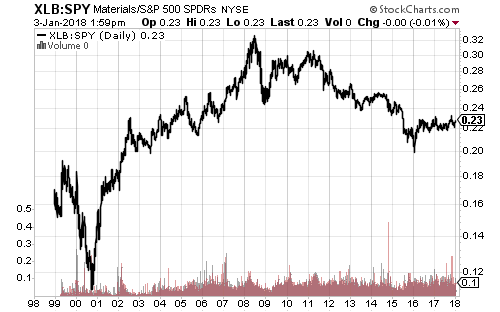

The materials sector was strong in 2017, but it hasn’t really outperformed the market since it bottomed in early 2016. Like energy, it sits at a relative price similar to the early 2000s. Materials will likely move with energy.