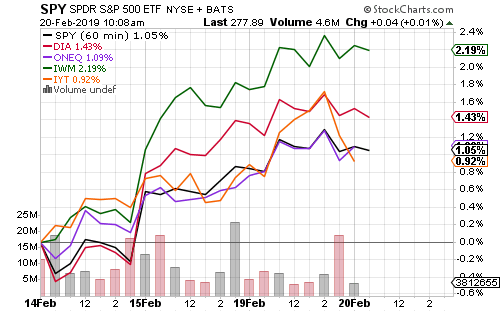

Equities continue to rally, with the Russell 2000 Index leading the way.

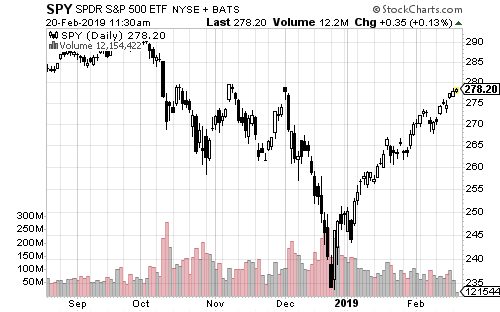

The S&P 500 Index is approaching recent resistance levels. This is the last line of major resistance for the index. We are now only 6 percent away from achieving a new all-time high.

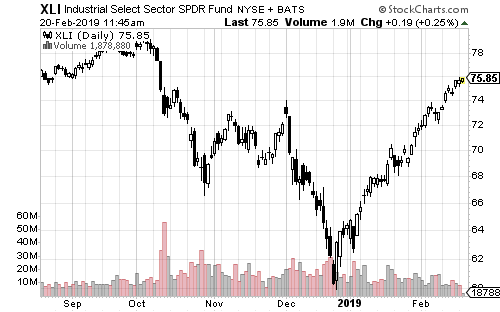

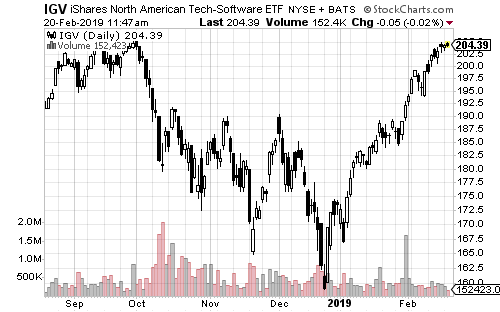

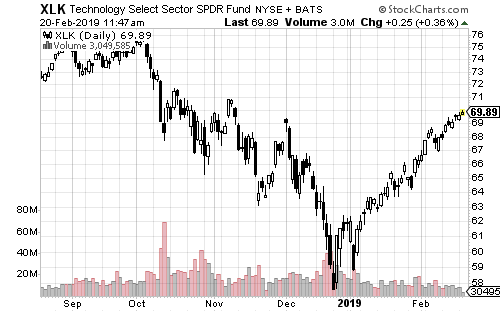

Industrials have already broken resistance levels, as has the software and semiconductor subsectors.

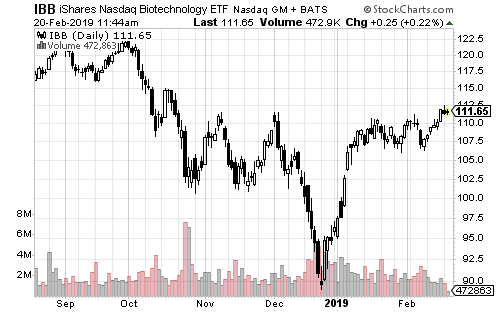

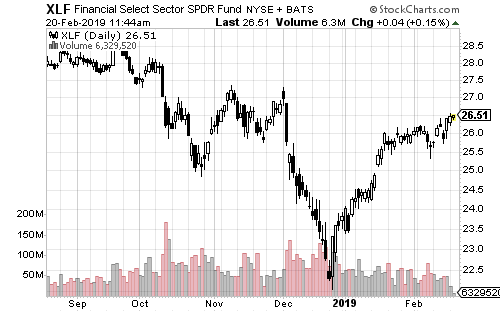

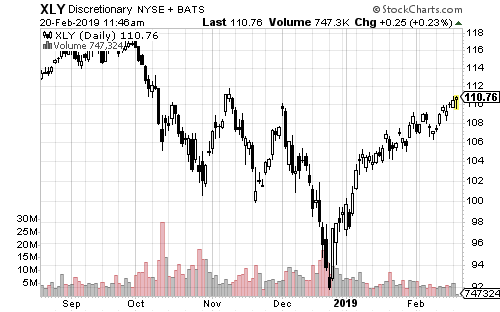

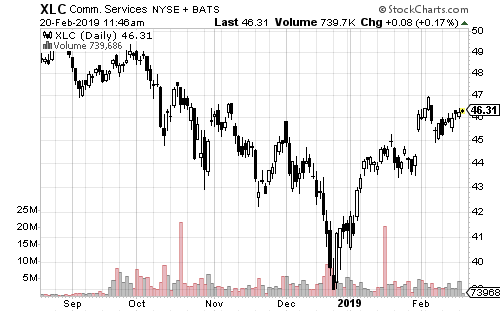

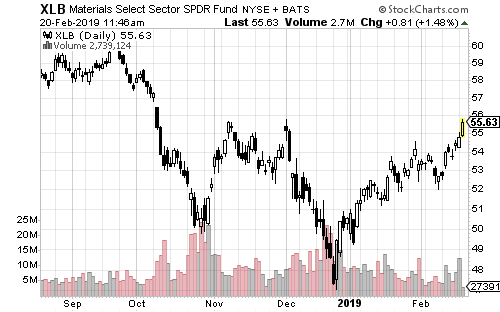

Healthcare, biotechnology, financials, consumer discretionary, communication services, materials and technology are on the cusp of a breakout.

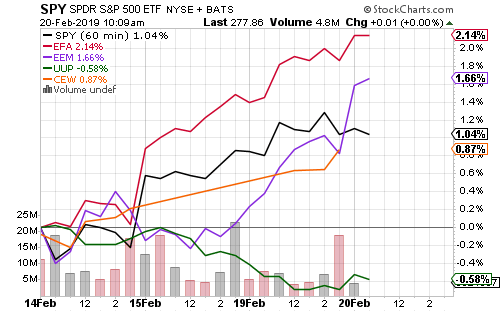

Developed and emerging markets outperformed in part to a weaker U.S. dollar and Chinese credit growth. This will bear watching in the next month as the Chinese Premier indicated no quantitative easing will occur.

The Chinese yuan has rallied after reports said the U.S. government demanded China not offset tariffs with a weaker currency. The bounce in the Chinese yuan lifted emerging market currencies, but it remains to be seen if this is a change in trend or political manipulation amidst trade negotiations.

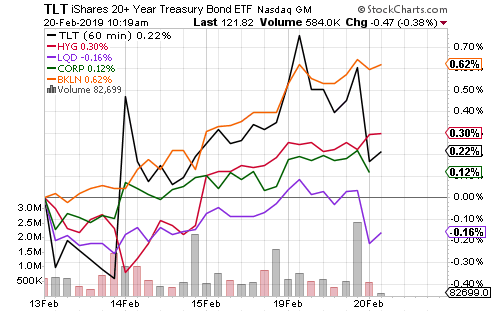

The Federal Reserve eased back on its rate hike forecast for 2019. Bond yields have been falling, lifting all categories of bonds. December interest rate futures show the market overwhelmingly believes the Fed will hold steady this year.

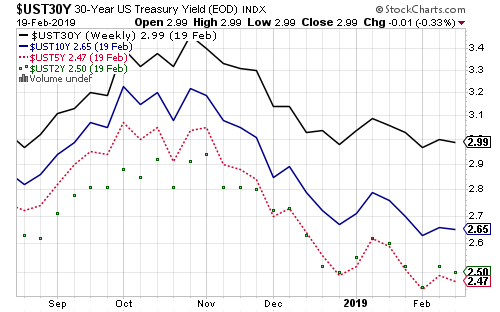

The Fed’s shift in tone has pushed the 5-year Treasury yield below that of the 2-year, an inversion of that part of the yield curve.