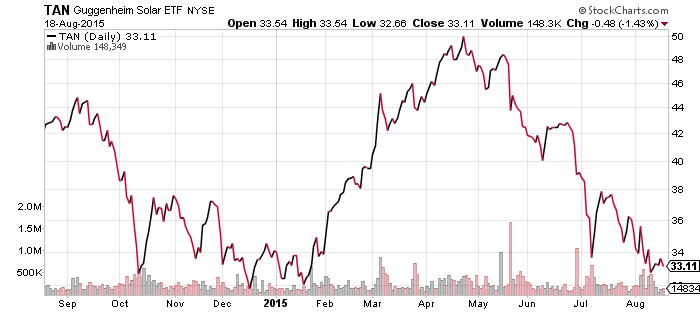

Guggenheim Solar (TAN)

TAN touched $50 in April after rising 50 percent over the course of three months. Over the next four months, it gave up all of its gains. Earlier in the year, the sector was hit by losses in a Chinese company, but lately it is energy prices pushing the sector lower. Solar is still years away from being a consistently competitive energy source and for now it relies on high energy prices to make it attractive to consumers. With oil prices near their 2009 lows, solar doesn’t look like a sound investment.

Going back 5 years show’s TAN is approaching an important support/resistance zone. Investors should expect a push well down into the $20s if it breaks $30.

WisdomTree Chinese Yuan (CYB)

PowerShares U.S. Dollar Index Bullish Fund (UUP)

WisdomTree Bloomberg USD Bullish (USDU)

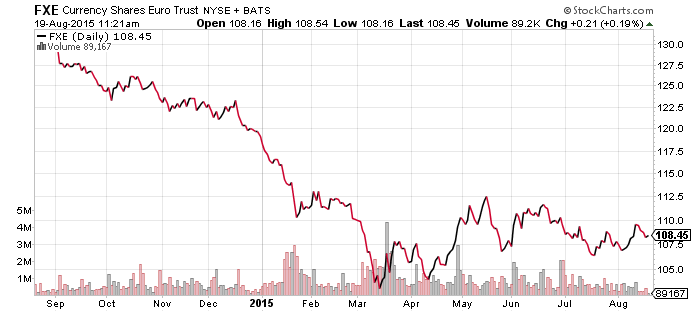

CurrencyShares Euro Trust (FXE)

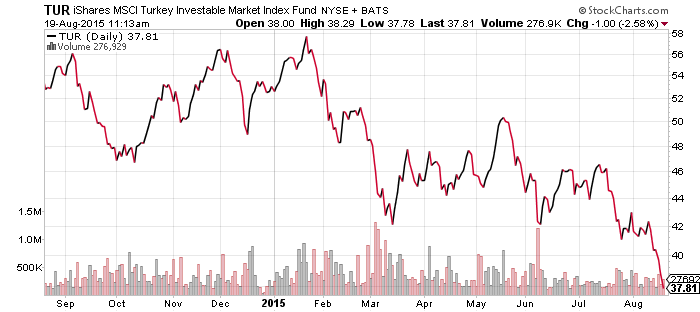

iShares MSCI Turkey (TUR)

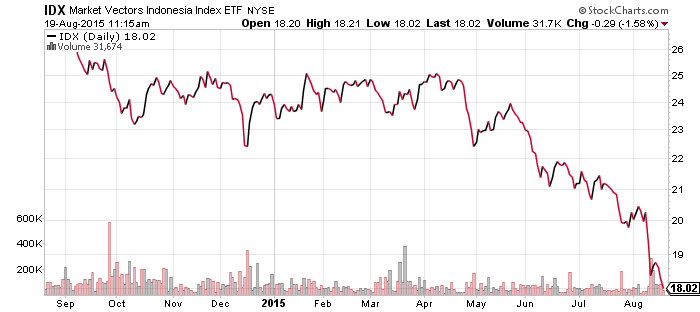

Market Vectors Indonesia (IDX)

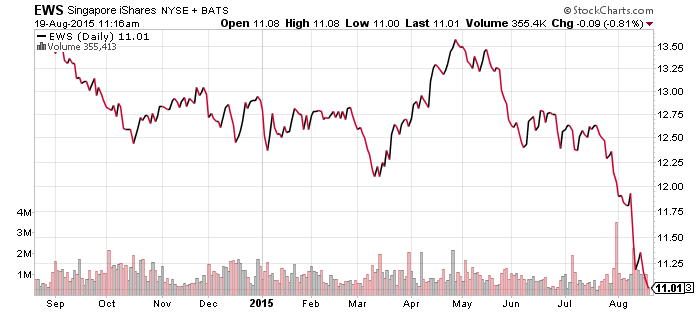

iShares MSCI Singapore (EWS)

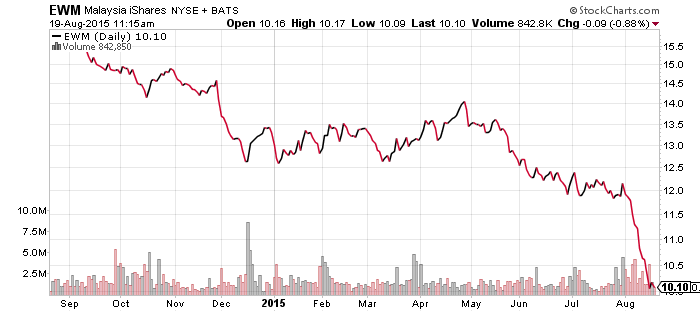

iShares MSCI Malaysia (EWM)

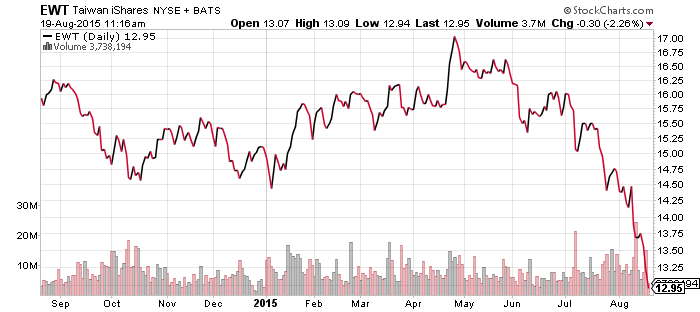

iShares MSCI Taiwan (EWT)

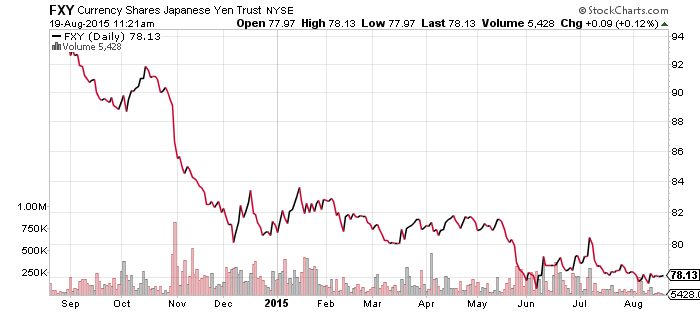

CurrencyShares Japanese Yen (FXY)

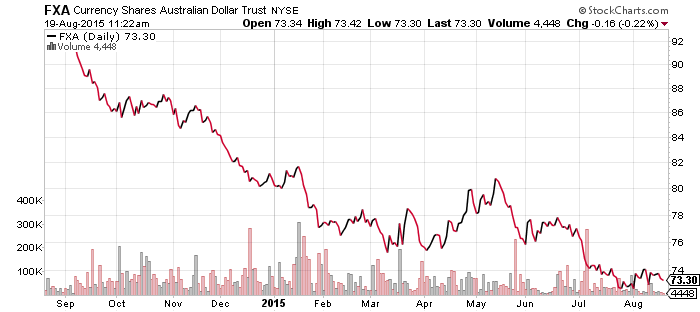

CurrencyShares Australian Dollar (FXA)

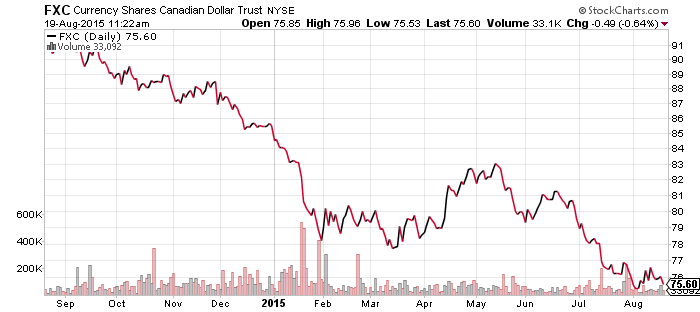

CurrencyShares Canadian Dollar (FXC)

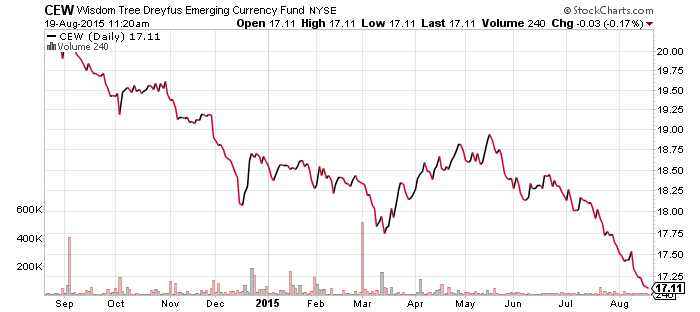

WisdomTree Emerging Market Currency (CEW)

Currency markets remain a center of attention in the wake of the yuan’s depreciation. Emerging markets currencies have yet to stabilize. Moreover, political trouble in Turkey has touched of a plunge in the lira. Malaysia’s currency has fallen back to late 1990s levels and Indonesia has similarly slid lower. Singapore and Taiwan’s stock markets and currencies have also declined sharply.

The Japanese yen remains unnaturally calm, almost flat lining in recent months. At least one official in Japan said the country can respond to yuan depreciation, which would almost certainly push the yen lower. However, it’s also possible that with emerging markets under heavy selling pressure, a bounce is due. The yen has remained stable for long periods in the past three years, punctuated by fast and sharp moves lower versus the U.S. dollar. Nothing may happen over the next week, but it’s a major currency for financial markets and close attention should be paid to it.

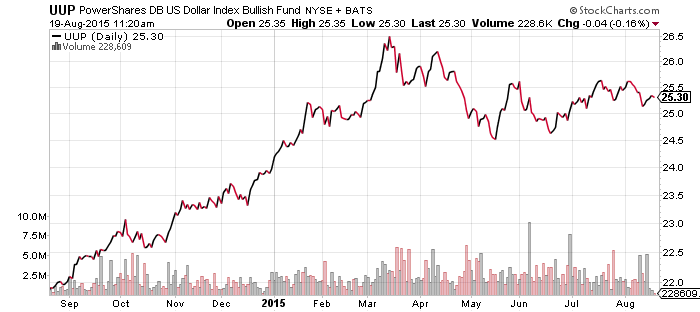

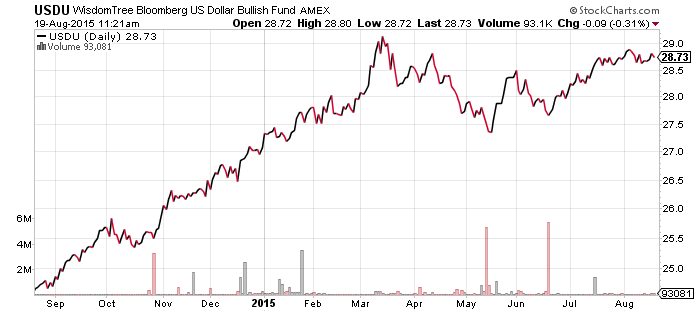

The U.S. dollar has been holding steady. A fund we have normally track, PowerShares U.S. Dollar Index Bullish Fund (UUP), has been declining a bit due to strength in the euro. WisdomTree Bloomberg USD Bullish (USDU) only has about a third in the euro and has been performing better. UUP only has exposure to the yen in Asia, while USDU has exposure to China and Australia, among others. Those latter currencies have been selling off, which is why the fund is much closer to its 2015 high.

SPDR Energy (XLE)

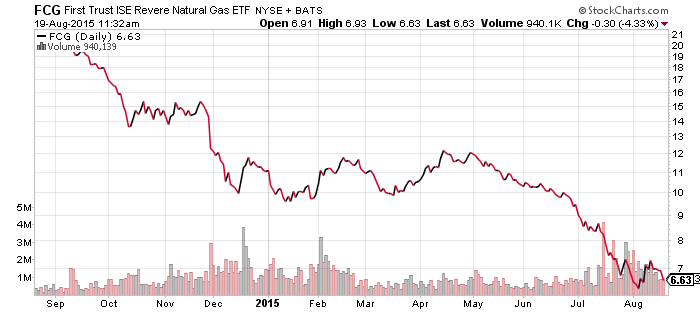

FirstTrust ISE Revere Natural Gas (FCG)

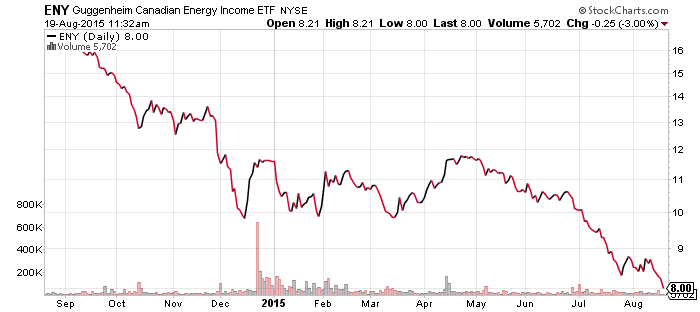

Guggenheim Canadian Energy Income (ENY)

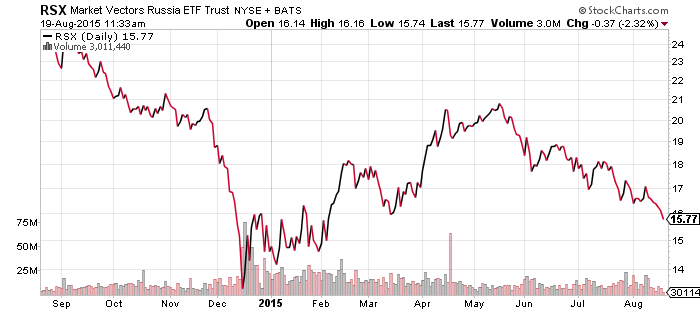

Market Vectors Russia (RSX)

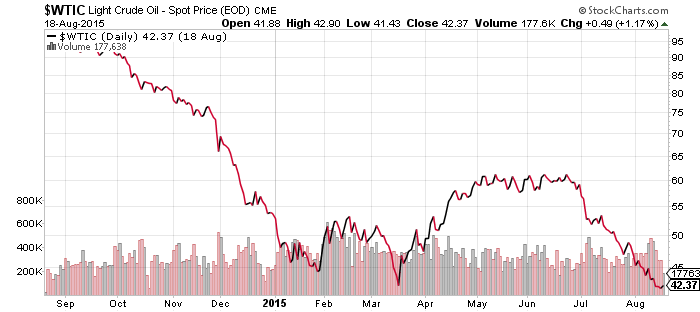

The oil market is at a major turning point. Oil inventories in the U.S. increased at their fastest pace in four months last week. Oil production has also fallen at the fastest pace since 2013. West Texas Intermediate Crude is at a new 52-week low and in a clear bear market, but has rebounded slightly. As the chart reflects, we are at a key support level and the only support is the 2009 low of $35 a barrel. Oil will be highly correlated with emerging markets over the coming weeks. Additionally, as oil prices fall, indebted nations and companies have greater incentive to pump as much as possible to stay solvent.

iShares iBoxx Investment Grade Corporate Bond (LQD)

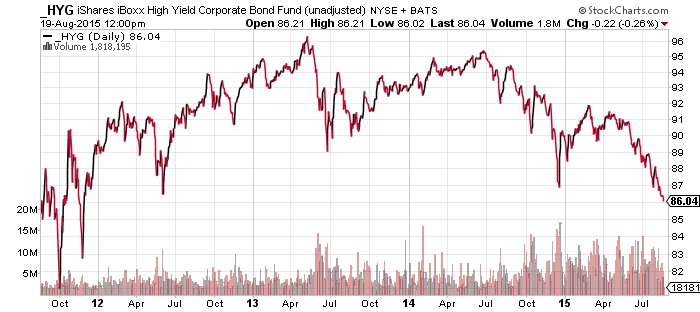

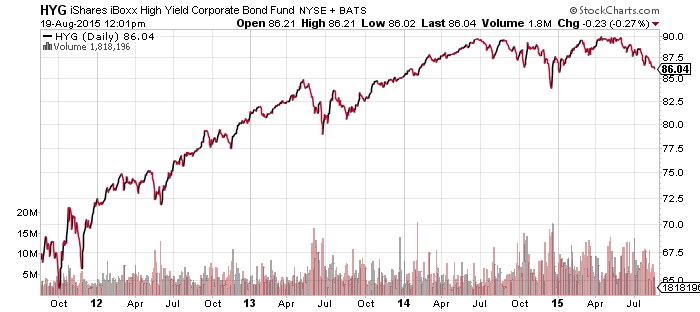

iShares iBoxx High Yield Corporate Bond (HYG)

The first HYG chart below is a price only chart, showing the price of the bonds in the portfolio, the second is the fund’s total return. As is clear, investors have done well holding HYG and the losses thus far in 2015 are small thanks to the hefty dividends. The price only chart makes it clear how much credit risk has been priced into the fund. Due to concerns about shale oil producers going bankrupt, the portfolio is priced at levels last seen in 2011, when the financial markets experienced a brief panic and equity markets corrected.

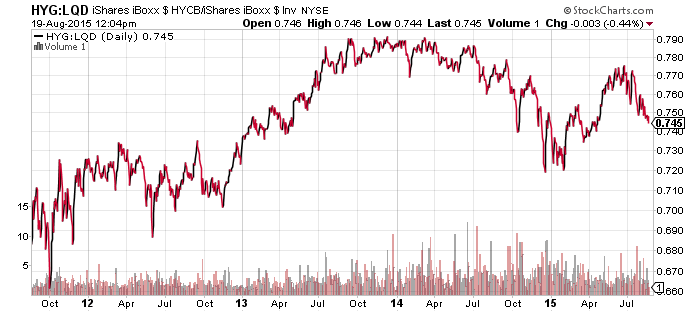

The last chart shows HYG is still outperforming LQD in 2015 thanks to its lower interest rate risk and those larger dividends.

SPDR Utilities (XLU)

SPDR Pharmaceuticals (XPH)

SPDR Materials (XLB)

SPDR Consumer Staples (XLP)

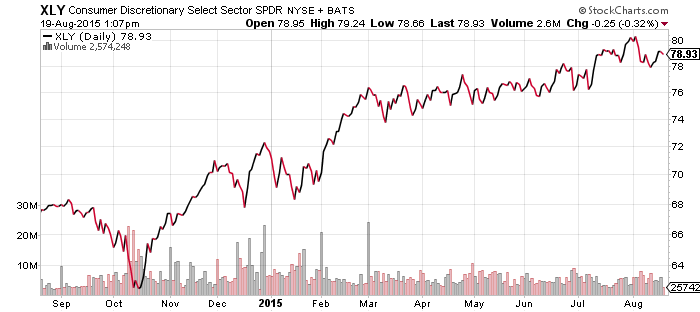

SPDR Consumer Discretionary (XLY)

SPDR Healthcare (XLV)

SPDR Technology (XLK)

SPDR Financials (XLF)

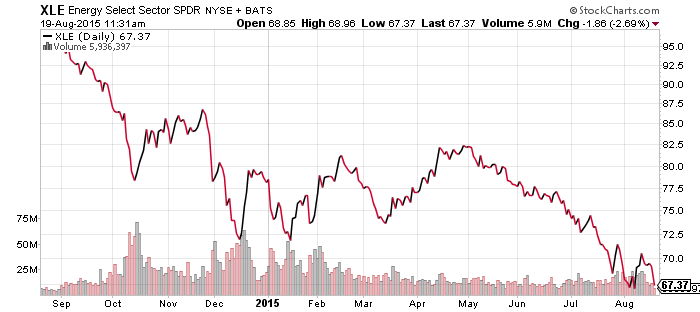

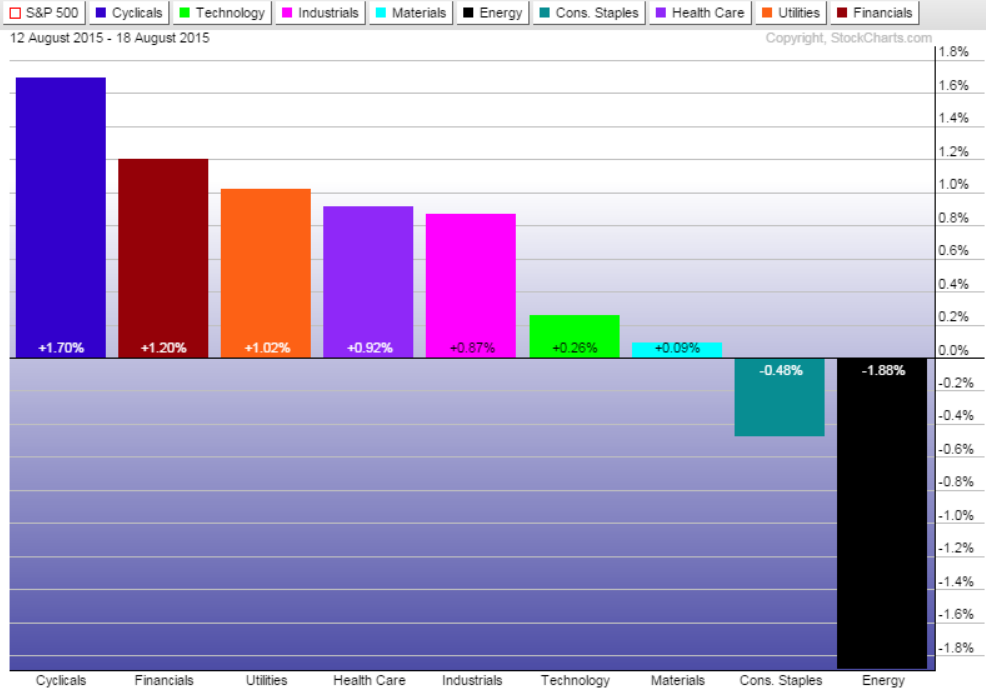

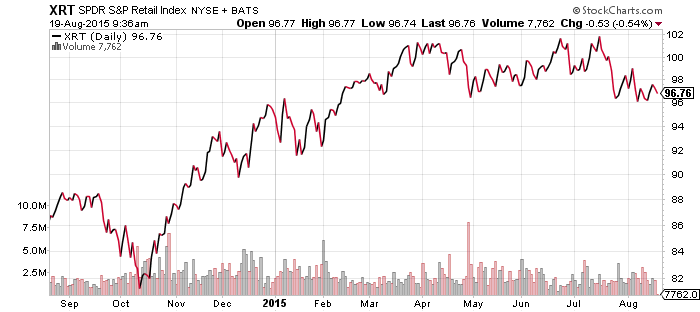

As you would expect from the drop in oil prices over the past week, energy was the worst performing sector, sliding nearly 2 percent. Consumer discretionary was the best performing sector, a bit surprising considering several retail firms disappointed investors with their earnings reports. XLY rose during the week, while SPDR Retail (XRT) was flat due to greater retail exposure.

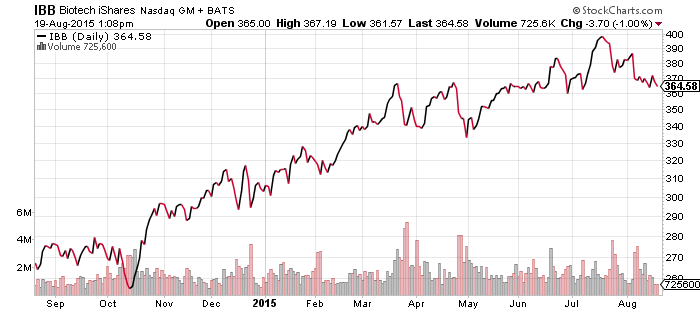

IBB is near support at $360 per share so a bounce is likely, but a breakdown would open up the risk of a drop to $340. SPDR Biotech (XBI) and First Trust Biotech (FBT) are both showing the same pattern in their charts.

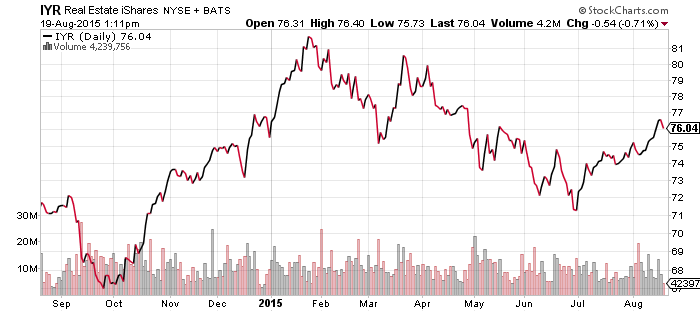

Rate sensitive utilities and real estate continue to rally as 10-year treasury yields drift lower.

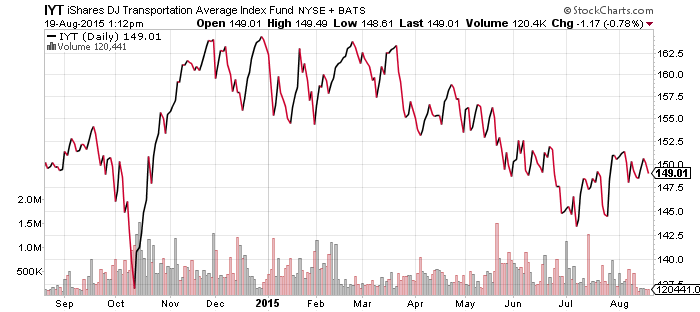

Transportation stocks also remain in an uptrend, a rally mainly due to rising airline stocks.

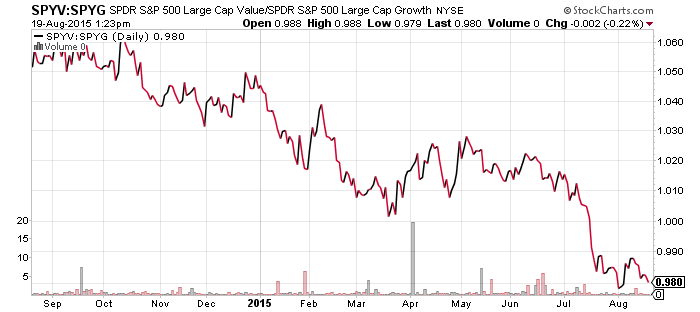

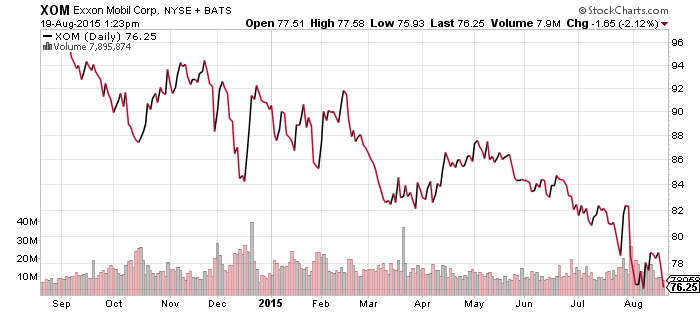

SPDR S&P 500 Large Cap Value (SPYV)

SPDR S&P 500 Large Cap Growth (SPYG)

The value versus growth ratio is testing its lows for the year. To illustrate what is at work here, look at the similarity between the ratio chart and the chart of Exxon (XOM). If oil prices slide further in the week ahead, both value and energy will move lower. Both Chevron (CVX) and ConocoPhilipps (COP) are already at new 52-week lows and XOM is likely to follow.

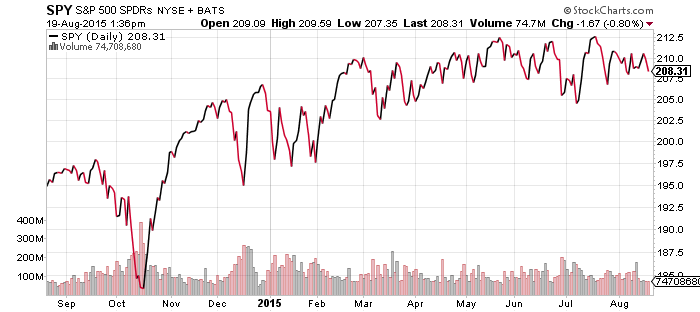

SPDR S&P 500 (SPY)

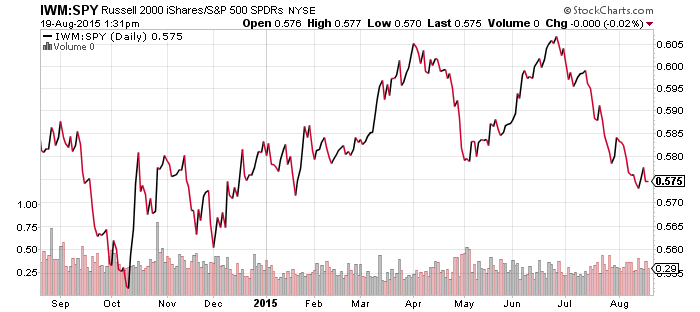

iShares Russell 2000 (IWM)

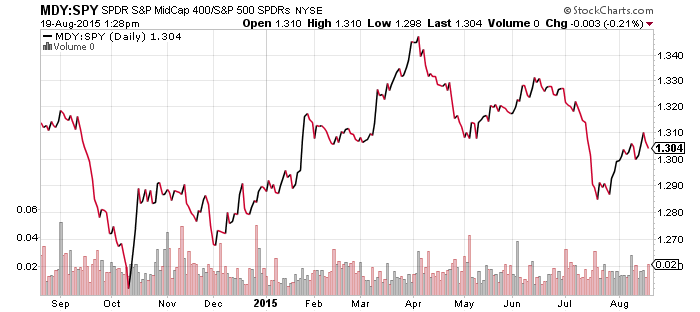

S&P Midcap 400 (MDY)

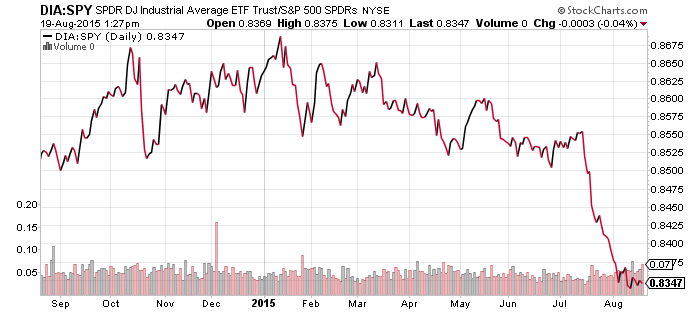

SPDR DJIA (DIA)

PowerShares QQQ (QQQ)

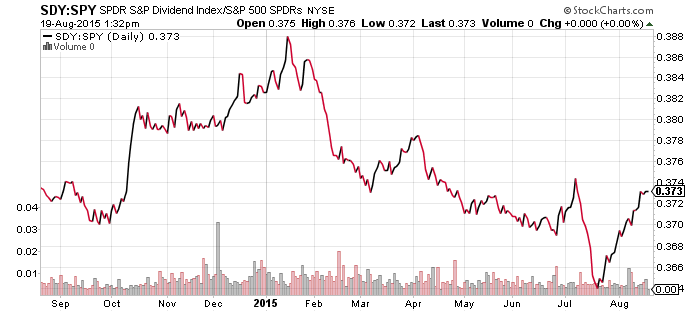

SPDR S&P Dividend (SDY)

The Dow stabilized relative to the S&P 500 Index over the past week. The Nasdaq has steadied as well, but is much closer to its relative highs for the year. Mid-caps remained in a relative uptrend, while small-caps continue to underperform. Dividend shares have rallied strongly relative to SPY since late July.

As for the broader market, it remains in a relatively narrow trading range. SPY has been in a $10 range (approximately 5 percent) between $202.5 and $212.50 since February.